For many small businesses, even profitable ones, the level of cash in the bank can be the difference between success and failure. Ensuring you know what you need in reserve – to meet your growth objectives or navigate bumps in the road – should be an integral part of SME business planning.

A recent Business Confidence Survey from Capify, found that the majority of SME owners are concerned about cashflow in their business.

On top of rising prices throughout the supply chain and the spectre of recession on the horizon, many SME owners are reporting a negative trend in the cash position of their businesses. Over half of the survey respondents (53%) were concerned about the levels of cash held by the business, whilst 43% report having less than $50,000 AUD in the bank (an increase of 6pp on Q4 2021).

So, what can business owners do to ensure they have the right level of cash in the bank? Our simple guide below will help you feel more comfortable about the reserves you need to facilitate growth or overcome cashflow hurdles, and guide on ways of increasing capital to meet these needs.

1. Be clear on this year’s business objectives

Every SME is different and there is no set answer for how much your business should have in cash reserve. The best approach is to tailor cash reserves to meet your business’ specific needs. Look at your 12-month trajectory and carefully work out your future goals and plan out your forecasts.

For those SMEs in growth mode, having larger cash reserves for investment in staff, machinery or inventory may be advisable. For those who are forecasting a year of consolidation, keeping a smaller reserve just in case you encounter any hiccups over the year might be more advisable. Either way, making sure that you have money in the bank and positive cashflow running through your business is what every SME should strive for.

2. Get to grips with your outgoings and calculate your reserve requirements

By working out how much your business needs to spend on average each month on things like rent, utilities, and other inventory costs, you can devise a plan for how much you need to keep in the bank in case of emergency or plans for growth.

Whether your expenses are typically quite consistent throughout the course of the year or not, there is a simple process to follow to work out your monthly expenditure. Use your accounting software or bank account statements to help:

- Take a look at your cash flow statements from the past 12 months (this will take into consideration any seasonal variations)

- Work out how much you spend each month (note down the biggest spending month as this will be useful to know for the future)

- Add all these together, divide by 12 and this will give you your average monthly expenditure

If you’re a seasonal small business, it means your expenses will likely be more concentrated in certain months aligned with your sales. It’s important to know when these times are, which is why using a period of 12 months is so beneficial.

3. Working out your reserve

If your business’ monthly expenses remain fairly consistent throughout the year, multiply your average monthly costs by either three or six, depending on how many months you want in your reserve.

For example: If your average monthly expenses are $20,000 AUD and you want a three-month reserve, your sum would be: $20,000AUD X 3. Therefore, making your cash reserve $60,000 AUD.

If yours is a more seasonal business you need to be saving enough to cover your one high month, but also those regular months in between.

Take a look at the following example to work out how much money to put in the bank as a seasonal business:

Say your high-cost month is A$80,000, your regular months are A$30,000 and you want a three-month cash reserve.

- Multiply A$30,000 by two months to get the total for the first two months = £60,000

- Add the A$80,000 high-cost month

- Your total of A$140,000 is your three-month reserve, which ensures a strong cash flow for one high month and two regular months

4. Build that cash reserve

There are a number of ways businesses can start to build their cash reserves. One option is to simply transfer a certain amount of your profits to a separate bank account or a savings account each month until you reach your ideal reserve amount.

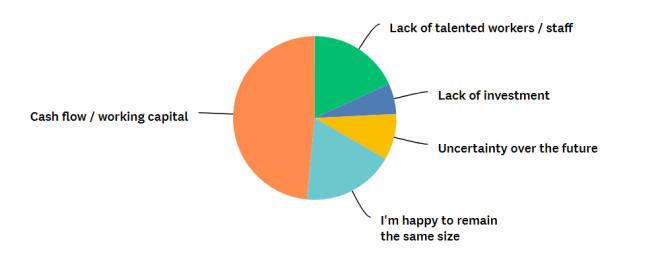

For many SMEs, who need to retain their monthly profits, self-financing isn’t an option. Indeed, 47% of respondents to Capify’s Q1 Business Confidence Survey identified working capital / cash flow struggles as the primary driver for seeking external finance.

There are several external funding options that can help you build your cash reserve without having to take funds away from other area.

5. Borrow money before you need it

The best time to solve a cash flow problem is before it happens. If your business is running smoothly or is in the beginning stages of production, now is the time to borrow money.

By taking a Small Business Loan when your numbers are good, you can avoid the risk of rejection later. This will also provide you with resources to fall back on should you experience any growing pains associated with starting a business. While businesses can run on a cash or accrual basis, Rohit Arora, CEO of Biz2Credit, advises every business to take advantage of both.

Whatever amount you think you will need, ask for double; you might not get it, but it’s better to have reserves to draw from when times get tough,” he said. “If you can get a Small business loan at 10% or less, your cost of capital will be so much lower than if you put purchases on credit cards that carry rates of 19% or more.

At Capify, we offer a range of low doc business loans to help support your business through high and low periods. Check to see if you’re eligible for one of our loans using our online application.

Or, if you’d prefer to talk to a member of our team, we’d be happy to guide you through the process. Give us a call today at 1300 760 930.